The world’s share markets had an eventful end to the third quarter, down at least in part to the fallout from UK’s ‘mini-Budget’.

The third quarter of 2022 ended in tumult for UK investors. The now departed third Chancellor of the quarter, Kwasi Kwarteng, produced a ‘mini-Budget’ on Friday 23 September that sent shock waves around the world throughout the following week. The Monday after the ‘mini-Budget’ – which he insisted was not a Budget at all – the Bank of England and HM Treasury were both forced to issue statements designed to calm jittery markets.

Two days later the Bank of England was in full fire-fighting mode as government bond (gilt) prices tumbled. To stem the falls, the Bank of England announced it would be spending up to £65bn to buy gilts over a period of 13 days. That message helped bring some stability but left many economists musing over the fact that six days previously the Bank of England had said it would be selling £80bn of gilts it owned over the coming year.

On the final day of September, the Chancellor and the Prime Minister, Liz Truss, held a meeting with the head of the Office for Budget Responsibility (OBR) to discuss an assessment of the not-so-mini-Budget’s economic and fiscal impact. The OBR had offered such a review before 23 September, but it had been rejected by Mr Kwarteng, a decision that contributed to the market turbulence and his short-lived tenure in the hot seat.

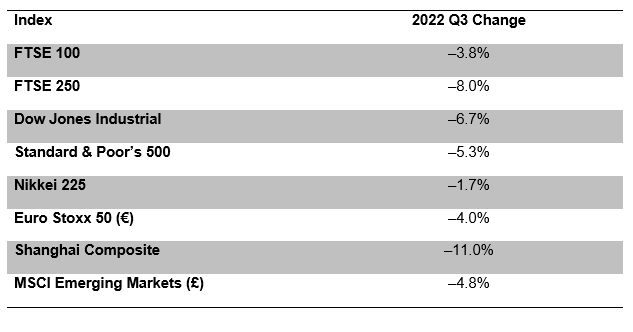

The dramatic ending to September left many investors thinking it must have been a terrible quarter. In fact, as the table shows, the most widely quoted UK market index, the FTSE 100, showed considerable resilience, declining by less than 4% over the three months. On the bald numbers, the FTSE 100 performed better than the US market yardstick, the S&P 500. However, that is not the case once currencies are considered. Over the quarter, the dollar appreciated by 9.0% against the pound – a mix of dollar strength and pound weakness. Adjust for this and a UK investor would have seen a sterling return on the S&P 500 of +3.2%.

The difference is a reminder of one benefit of investment diversification that can be forgotten – it can spread beyond just investments markets to include currencies. With further fall out following the reversal of many financial measures put in to place, we wait to see what the knock on effect will be for quarter 4.

To discuss your financial planning, contact our Sheffield based Financial Advisers on 0114 266 4432 or info@smh.group

Comments are closed.